Thinking about an electric car? The UK EV Salary Sacrifice Scheme might be your cheapest route. Many employers now offer this popular benefit. It lets employees drive a brand-new electric vehicle (EV) for less money each month.

But how does it really work? And who benefits most – you or the lease company? Let’s break it down.

How the EV Salary Sacrifice Scheme Works

The idea is simple. You agree with your employer to give up part of your gross salary. In return, you get the use of a new electric car.

- Choose Your EV: Your employer partners with a lease provider. You pick an EV from their range.

- Salary Reduction: Your employer deducts the monthly lease cost from your salary before tax and National Insurance (NICs).

- Tax Savings: Because the deduction is pre-tax, your taxable income is lower. This means you pay less income tax and fewer NICs.

- Company Car: The car is technically a company car leased by your employer for you.

Government Backing Makes it Cheaper

The UK government wants more people driving electric cars. They use tax rules to encourage this.

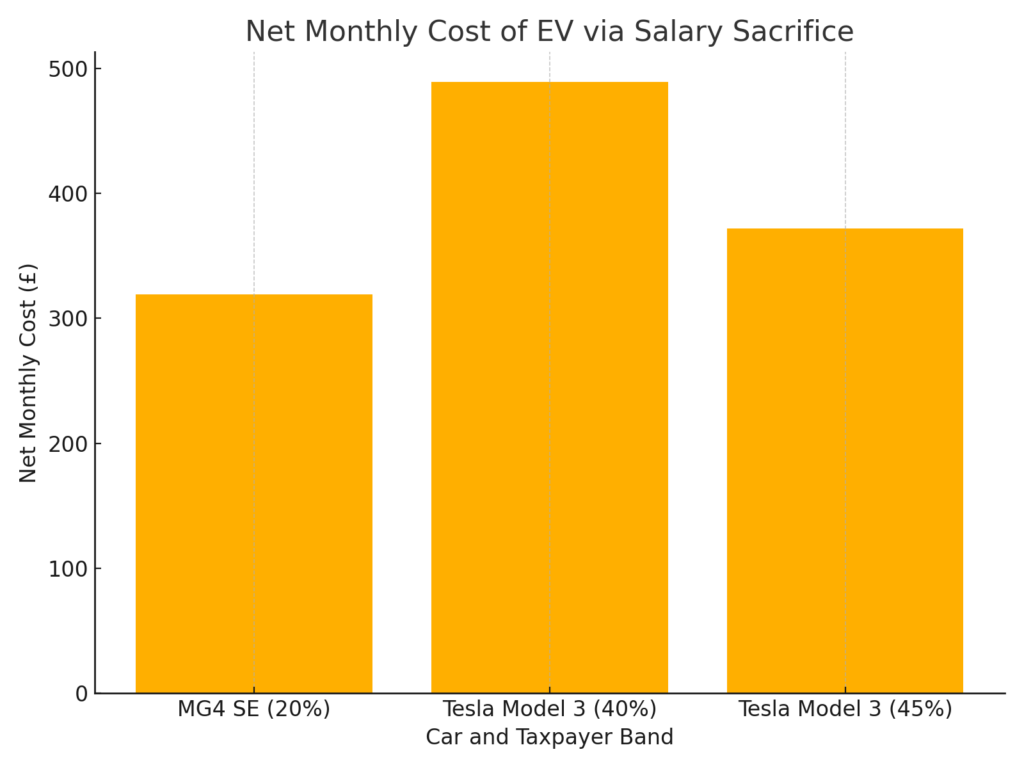

- Low Benefit-in-Kind (BIK) Tax: EVs have a very low BIK tax rate. Currently, it’s just 2% (until April 2025). Even planned rises (up to 9% by 2030) are much lower than petrol/diesel cars (up to 37%). This low BIK tax is crucial. It ensures the tax you pay on the benefit doesn’t wipe out your salary sacrifice savings.

- Favourable Rules: The government specifically supports EV salary sacrifice. It’s excluded from tougher rules applied to other salary sacrifice benefits.

Your Financial Benefits: Real Savings

The biggest win for employees comes from tax savings.

- Lower Income Tax: Paying the lease from pre-tax salary reduces your tax bill.

- Lower National Insurance: Your NICs are calculated on the lower, post-sacrifice salary.

- Significant Savings: These savings can add up to hundreds of pounds monthly. This often makes salary sacrifice much cheaper than leasing an EV personally (using post-tax income). Higher-rate taxpayers usually save the most.

- VAT: Your employer handles the VAT on the lease. They can usually reclaim 50% of it. This can help lower the overall cost offered to you.

What About the Lease Companies?

Lease companies run these schemes for employers. They handle vehicle sourcing, administration, and often bundle services.

- All-Inclusive Packages: Many schemes include insurance, servicing, maintenance, breakdown cover, and sometimes tyres or home chargers. This adds convenience and value.

- How They Make Money: Lease companies profit through fleet discounts from manufacturers, reclaiming some VAT, the lease payments themselves, and charges for bundled services or early termination.

- Competition Helps You: Many providers exist. This competition helps ensure schemes offer good value to attract employees. Transparency is key – always check the quote breakdown.

Salary Sacrifice vs. Other Options

- vs. Personal Leasing (PCH): Salary sacrifice is usually significantly cheaper monthly (often cited as 20-60% savings) due to the pre-tax advantage.

- vs. Buying: Salary sacrifice avoids a large upfront cost. It also usually includes running costs (insurance, maintenance) in one payment. You don’t need to worry about the car losing value (depreciation).

Important Things to Consider (Potential Drawbacks)

While attractive, be aware of potential downsides:

- Lower Net Pay: Your take-home pay will decrease. Ensure you can still comfortably afford your living expenses. Your pay must not drop below the National Minimum Wage.

- Pensions: It could affect contributions/payouts, especially for final salary (defined benefit) pensions. Check with your pension provider.

- Mortgages/Loans: Lenders look at gross income. A lower sacrificed salary might affect borrowing capacity.

- Leaving Your Job: Ending the lease early if you leave your job can trigger large fees. Check the scheme’s protection clauses (e.g., for redundancy).

- Insurance Excess: Even if insurance is included, you’ll likely have an excess to pay if you claim.

- Car Choice: The scheme might offer fewer models than the open market.

Real-World Success

Many UK companies and even public sector bodies (like county councils) successfully use these schemes. Employees report significant savings and value the benefit. This shows the scheme genuinely delivers for employees in practice.

Conclusion: A Great Deal for Many Employees

The UK EV Salary Sacrifice Scheme offers real, substantial financial benefits. The government’s tax incentives are designed to directly help employees adopt electric cars affordably.

Lease companies are essential partners, but the structure heavily favours employee savings. The convenience of bundled packages adds further appeal.

However, it’s not automatic savings for everyone. You must check the impact on your net pay, pensions, and borrowing. Understand the early termination risks.

Bottom Line: If you weigh the pros and cons carefully for your situation, EV salary sacrifice is often the most cost-effective way to drive a brand-new electric car in the UK. Research your employer’s scheme and compare quotes thoroughly.